The only way is up

01 March 2017

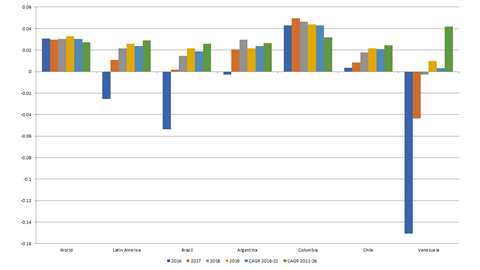

Total construction spending for key markets (Percent change, Real US $2010)

While the global economy is gradually improving, progress will be slow for Latin America. On the positive side, Peru, Chile and Colombia will benefit from sound fiscal and monetary policies, trade alliances and a modest rise in commodity export revenues. Argentina’s medium term outlook has improved under President Mauricio Macri’s reforms, but high inflation and fiscal deficits remain challenges. Brazil’s recession is slowly abating as inflation and interest rates come down, but conditions for a rebound are not yet established. Venezuela remains in something of a downward spiral, with huge deficits, hyperinflation, shortages and plummeting investment. Across the region, long-term challenges include inadequate infrastructure, restrictive business environments and a good deal of income inequality.

Brazil’s three-year economic contraction is easing, but its long-term growth crisis will likely continue. The country remained in recession as 2016 ended, although industrial production shows signs of stabilising. Even so, the Purchasing Managers’ Index (PMI) remains in contraction, and Brazil’s PMI is among the lowest of the nearly two dozen countries for which IHS Global compiles PMI data. Inflation is easing, enabling the central bank to reduce interest rates, and the government is making progress enacting fiscal austerity. Yet widespread corruption and low oil prices have taken a heavy toll on the energy construction and financial sectors. Consumers are not in a position to boost the economy – employment and real wages are declining and debt burdens are high. High taxation, local content regulations, administered prices and infrastructure bottlenecks continue to hurt competitiveness. Investment will drive a limited recovery – firms need to replace worn-out equipment and replenish inventories. Economic activity has benefited from a limited recovery in the mining and metallurgical industries. However, this recovery remains hostage to global mineral prices, and without a boom in primary commodity prices, growth potential is limited. We expect essentially no growth in 2017, with a mild recovery to 1.7% GDP growth in 2018. In the longer term, we expect Brazil’s growth to lag behind most of its rivals in the region by a considerable margin.

Commodity prices drive many of the region’s economies, and since late October, non-oil commodity prices measured by our IHS Materials Price index are up 5.5%. The US election had a role, but prices had been moving higher on optimism for better demand growth. Now, markets look overbought. It is China that matters most; US consumption for most commodities is only about one-fifth of Chinese consumption. We expect only a modest increase in US infrastructure spending, and that one to two years from now. While China seems to have an implicit guarantee to support industry, its manufacturing sector continues to slow. We expect continuing cuts in exploration and development budgets will gradually tighten supplies and put upward pressure on prices, but the modest pace of demand growth means prices are unlikely to rise much in the short term.

In Argentina, real GDP growth fell 2.1% in 2016, following 1.4% growth in 2017. High inflation, fragile public finances, social polarisation, a weak institutional framework, and high volatility in commodity prices are major issues facing the country. The Argentine economy is expected to rebound slightly in 2017, growing 1.4%, before reaching 2.1% growth in 2018. Argentina’s birth rate is declining, while its over-65 population is growing. As a result, the over-65 cohort will account for the largest share of the population in coming years. Conditions to attract investment remain weak, limiting productivity growth and construction opportunities.

Despite low oil prices and economic deceleration, Colombia is expected to achieve 2.4% growth in 2017. Growth will be driven by private consumption and investment (30% of GDP during 2014). The implementation of the infrastructure programme should also boost the economy. The challenge for Colombia is that lower oil prices keep forcing it to make adjustments to manage its economy with decreased investment flows to the sector, lower oil export revenues, and less money in state coffers.

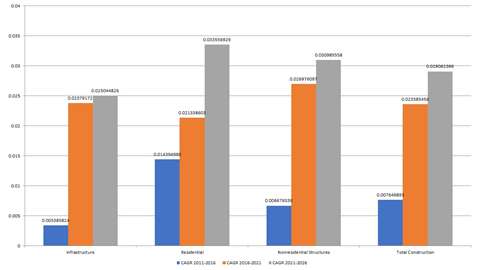

Real construction spending growth slows across all structure types

Peru and Chile will continue their recoveries, although commodity prices (mainly copper) will preclude a strong rebound. Sound macroeconomic fundamentals and a dynamic domestic economy will drive further expansion of these two economies during 2017 and especially 2018 and beyond.

Lagging behind

The relative strength of Latin America compared with the world is evident in Figure 1. Latin American construction spending will expand once more in 2017, but post gains at below global rates over the medium-term forecast. Brazil combines with Venezuela to hold back the outlook, and, of the major economies, only Colombia grows at above world average rates.

The timing of Chile’s political cycle, broad tax and education reform, changes to labour-market and pension legislation, low copper prices and a less favourable mining investment cycle have weakened consumer and business confidence, challenging the construction sector. Ecuador has cut public investment into infrastructure in response to falling oil revenues. We expect a modest recovery as commodity prices rebound and show moderate growth in 2017, then improve further in 2018.

Infrastructure spending, vitally needed to advance the region’s economies, has borne the brunt of the slowdown as fiscal problems limited public investment. Brazil, Ecuador, Uruguay and Venezuela all reduced spending in 2015 and 2016, and are unlikely to reverse that trend in 2017. Apart from Venezuela, growth will return, but it will be limited. Infrastructure construction is the largest construction component in Latin America, accounting for almost half of construction spending in the region. Brazil and Argentina have the largest markets for infrastructure, and are among the most exposed to economic slowdown and fiscal challenges. Thus, infrastructure spending for the region will average 2.4% growth over the next five years, roughly in line with total construction market growth.

The growth leader is non-residential construction. However, even this structure type will see barely 2.7% growth as weakness in commodity prices, depressed business confidence and diminished investment opportunities keep new expansion plans on hold for a couple of years.

Latin America faces significant challenges in the near term, and the largest markets will be the most impacted. Of the major economies, only Colombia could be considered to have a strong market. There is potential in some smaller economies, such as Peru and Ecuador, particularly if oil prices stabilise, but they will have insufficient mass to advance the region. The situation is particularly grim for heavy equipment as cuts to infrastructure combine with weakness in mining and energy to limit potential.