Outlook for construction in Western Europe

09 January 2023

Scott Hazelton of IHS Markit lays out a somewhat bleak economic future for the economies and construction markets of Western Europe

The war in Ukraine, energy supply and price issues, plus tighter financial conditions to fight inflation broadly will tip the eurozone economy into recession in late 2022 and early 2023.

Construction work being carried out on a site in Frankfurt, Germany. (Photo: AdobeStock)

Construction work being carried out on a site in Frankfurt, Germany. (Photo: AdobeStock)

Although major governments have rolled out packages to shield households and firms from surging energy prices, high inflation will take a toll on confidence, spending and investment decisions.

The European Central Bank’s (ECB) tightening monetary policy will add further financial strain on households and firms.

These developments will translate into further weakness for Western European construction.

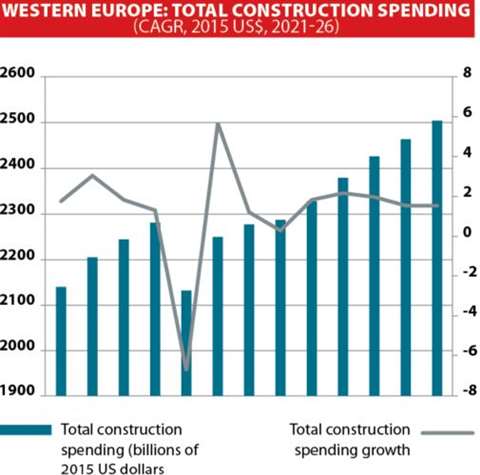

Western European construction spending

German construction firms signalled the quickest contraction in activity, as the headline index hit a 19-month low.

Both Italy and France reported softer reductions during the latest survey period, while construction activity returned to growth in the United Kingdom.

Activity fell across all three subsectors, but homebuilding registered the quickest reduction. Civil engineering and commercial construction activity fell for the sixth straight month, although the rates of contraction softened.

We expect real total Western European construction spending to rise by just 1.2% in 2022.

With headwinds set to linger into 2023, and as the ECB’s rate hikes start to bite, construction spending is expected to rise just marginally next year, by only 0.4%.

After a weak second quarter, with German real GDP rising by just 0.1% quarter on quarter (q/q), the Russia–Ukraine war and effective halt to Russian gas deliveries at the end of August will almost inevitably tip the economy into recession during the next two to three quarters.

Germany’s inflation rate reached double digits for the first time in September and tighter ECB monetary policy will erode consumers’ disposable income, despite government support measures.

Fixed investment already fell by 1.3% q/q in the second quarter of 2022, largely due to construction, which recorded a quarterly fall of 3.4%.

Leading indicators such as the ifo Business Climate Index and the PMI point to further weakness in the second half of 2022.

Total construction spending in Western Europe. (Photo: IHS Markit)

Total construction spending in Western Europe. (Photo: IHS Markit)

We expect total construction spending to decline by 0.9% in 2022, followed by a further decline of 1.8% in 2023, even as the government pushes ahead with infrastructure investment to reduce dependence on Russian energy.

Rising inflation and interest rates will dampen housing affordability and household demand for home improvements.

Risks of energy shortages, further increases in energy prices, tighter financial conditions, and uncertainty relating to the war in Ukraine will cause delayed investment in non-residential structures.

Commercial construction activity in Italy

Italy is also likely to slide into a recession in the final quarter of 2022 and early 2023 given growing headwinds.

Yet, temporary support measures rolled out by the government are expected to cushion the impact of energy price hikes on households and firms during the second half of this year.

In addition, Italy is the largest recipient of grants and cheap loans from the European Union’s Recovery and Resilience Facility (RRF), providing a boost to private-sector investment to finance major public projects, particularly in infrastructure.

We have total annual output in Italy increasing by 2.5% in 2022, followed by a further 2.8% in 2023.

Italian construction companies signaled a third successive monthly reduction in overall activity during September, according to PMI® survey data.

Across the three broad sectors, housing and civil engineering registered softer contractions compared with August.

At the same time, commercial construction activity rose for the first time since July.

Construction activity in France declines

Construction activity across France continued to decline in September, according to the latest PMI survey, but the rate of contraction was the softest over the current four-month sequence amid varying trends across subsectors.

Housing signalled a marked decline in activity that was the steepest in three months. Civil engineering activity also contracted, though the rate of decline was only marginal, while commercial activity increased slightly.

Demand followed a similar trend, with the seasonally adjusted new orders index scoring only marginally below the 50.0 no-change threshold to signal a mild fall in sales.

Although France is less dependent on Russian gas than some of its neighbours, more than half of its 56 nuclear reactors have been shut down for maintenance, forcing a reliance on imports just as an energy crisis is looming.

As a result, our macroeconomic forecasts see France entering recession in late 2022 or early 2023, despite the governmental measures to cap energy prices.

Overall, real total construction spending in France is forecast to rise by 2.2% in 2022, before flattening to 0.1% in 2023.

How will UK construction perform in 2023?

Selected construction spending of countries in Western Europe. (Photo: IHS Markit)

Selected construction spending of countries in Western Europe. (Photo: IHS Markit)

The UK experienced lacklustre performance during the second quarter of 2022, with real GDP rising by only 0.2% q/q.

Construction was a key driver of activity and was the only sector to record continued growth in July and August.

The Office for National Statistics data showed that the volume of construction output rose by 0.4% month on month in August, up from 0.1% in July, when warmer-than-average temperatures made working conditions difficult.

UK construction firms signalled a rise in overall activity in September following two months of decline, according to latest PMI® data.

Housing was the best-performing sector, with activity levels rising at the fastest rate in five months, while commercial activity also expanded.

In contrast, civil engineering registered a third consecutive monthly decline in activity, albeit at a rate that was the softest seen over this period.

Inflationary pressures remained sharp but the rate of input price inflation moderated slightly.

Weak economic growth, ongoing Brexit tensions, and the end of the government’s super-deduction scheme on 31 March 2023 will drag on business investment.

Against this backdrop, real total construction spending in the UK is expected to rise by 1.5% in 2022 but decline 0.4% in 2023.

The chart above indicates the medium-term outlook for construction by country. The relatively short and shallow recession precludes any large downturns, but it also features and anaemic recovery.

Importantly, while the broad Eurozone will experience recession in 2023, there will be individual national exceptions.

The brunt of the downturn will be felt by economies that are relatively manufacturing intensive.

Norway escapes the downturn as it is not as impacted by high energy prices. Greece and Spain benefit from large tourism sectors which, while negatively impacted by recession, see more than offsetting gains from post-pandemic resumption of travel.

Ireland will see some challenges with its residential market, but broadly benefits from relocations due to Brexit.

These economies will be relatively strong, even in 2023, with consequently stronger prospects.

About the author

Scott Hazelton is a director with the Global Construction team at the market analyst IHS Markit.

Scott has over 30 years’ experience in construction, heavy equipment, building materials and industrial manufacturing markets.

CE Barometer – Market confidence continues to fall – CE October 2022 survey results

The CE Barometer survey for October was undertaken during the first three weeks of November.

Construction professionals from across Europe took part in this month’s CE Barometer survey.

The overall climate figure for this month’s barometer has dropped from 3.2% to 1.1% - this is a steep decline from August’s 14%.

This may demonstrate that, confidence levels can pick up in consecutive months, but can then drop again, seemingly inexplicably – suggesting that the waters ahead are still uncertain.

Breaking this down, we look first at business levels in October, compared with September and find that the majority of respondents (48.3%) report that they are unchanged.

August saw a considerable disparity between businesses’ that reported an uplift in business levels compared to those in a worse situation. The October results are less optimistic as 27.6% reported better business whilst 24.1% recorded that it was worse than the previous month.

Comparing today’s business levels with those a year ago, things are slightly more positive. Business is recorded to be better by 37.9% of respondents – a small increase from the previous month’s results.

Unfortunately, looking ahead 12 months, it isn’t quite so optimistic, with 37.9% of respondents anticipating worse levels of business.

The balance figure stands at -6.9% and suggests that with the European market full of ongoing challenges, many are less than optimistic about how business levels will pan out in the future.