Demand drops, United to curtail capex

30 April 2020

As United Rentals reports a large drop in rental demand following the Covid-19 outbreak, the company has said it expects its capital expenditure for 2020 to be significantly down year-on-year.

However, United has expressed confidence about its ability to weather the storm.

Matthew Flannery, CEO of what is the world’s largest rental firm, said, “While we’ve withdrawn our guidance at this time, we’re confident in our ability to leverage the resiliency inherent in our business model.

“We’re in the strongest position in our history to respond to this crisis and to prepare for the recovery to come. This includes the strength of our balance sheet and cash flow, as we remain focused on disciplined capital allocation and cost management.

“We expect our free cash flow to remain substantially positive in 2020, even in our worst-case scenarios.”

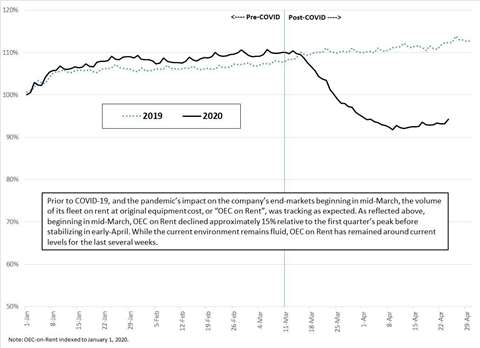

Prior to mid-March, the company’s first quarter performance was largely in line with its expectations, though this quickly changed in mid-March with the onset of the Covid-19 pandemic, as illustrated by the graph.

Total revenues in the first quarter were up 0.4% to $2.125 billion. Within that, rental revenues decreased by 0.7% to $1.783 billion.

Rental revenues had been slightly up year-on-year through February, before the crisis began in March.

Profits also took a hit, with adjusted EBITDA (earnings before interest, taxes, depreciation and amortisation) dropping by 0.7% year-on-year to $915 million. Adjusted EBITDA margin decreased 40 basis points to 43.1%.

A 2% year-on-year decrease in revenues in the general rental segment was attributed primarily to Covid-19.

Meanwhile, revenues in United’s specialty rentals segment – Trench, Power and Fluid Solutions –increased 4.6% year-on-year, including an organic increase of 2.8%. United acquired BlueLine towards the end of 2018. The segment’s increase in rental revenue reflected a 9.8% increase in average OEC (original equipment cost), partially offset by the impact of Covid-19 that began in mid-March.

United’s fleet productivity decreased by 1.2% year-on-year, again due to the impact of the pandemic in March, when rental volume declined. Prior to that, it had been on a par with the equivalent quarter in the previous year, and in line with expectations.

Although the great uncertainty caused by the pandemic has prompted United to withdraw its full-year 2020 guidance, Flannery said, “The modifications we’ve made to our operating protocols preserve our ability to serve the needs of thousands of communities, while retaining critical capacity for the return of end-market demand.”

Mitigating the impact of Covid-19

In early-March, United initiated contingency planning ahead of the impact of Covid-19 on its end-markets. This planning has focused on five key work streams that are the basis for the company’s crisis response plan.

The first is to ensure the safety and wellbeing of employees and customers. United has introduced various safety measures, from the provision of personal protective equipment to the increased disinfecting of equipment and facilities.

The second is to leverage the company’s ability to continue supporting the needs of its customers. All of United’s depots in the US and Canada have remained open, along with seven of its 11 European depots. Customers have been able to perform fully contactless transactions using United’s online services.

Disciplined capital expenditures is another key element. Although the current environment remains fluid, the company expects that its 2020 capital expenditure will be down significantly year-on-year.

United is also exercising tight control of its core operating expenses. Since March, the company has significantly reduced overtime and temporary labour, primarily in response to the impact of Covid-19. It has also reduced the need for third-party delivery and repair services, and minimised discretionary expenses across general and administrative areas of the business.

Finally, United is managing its balance sheet with a focus on liquidity. Asa a result, its share repurchase programme was paused in mid-March. As of the end of March, United’s total liquidity was just over $3 billion. The company has no long-term debt maturities until 2025.