Residential vs. non

15 April 2008

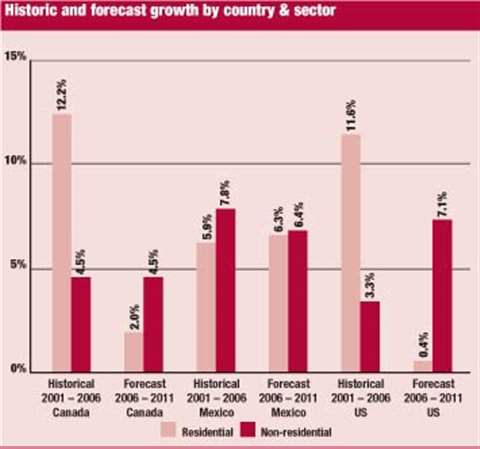

The near-term outlook for the North American construction market is dominated by the net effect of different cycles in the residential and non-residential markets. Both the US and Canada are seeing downward corrections in their housing markets, while non-residential structural investment growth has been strong. Mexico on the other hand will see a stable relationship between the residential and non-residential segments, but its impact will be dwarfed by its economically larger neighbours.

The US residential market has already declined significantly from its cyclical peak, due to escalating house prices that eroded affordability and led to supply outstripping demand. The problem has been compounded by increasing defaults in the ‘subprime’ mortgage market - lending to people with poor credit histories. This will increase the inventory of unsold homes further by forcing lenders to tighten their criteria, depressing home prices further.

Housing starts have a bit further to fall, but will turn the corner in 2007, although home sales will not recover until 2008. A weak market has been made worse by insurance companies, which are cutting back on writing new homeowners’ policies in states threatened by hurricanes.

In contrast, US non-residential construction rebounded in 2006, boosted by rising utilisation rates, falling office vacancy rates and post-hurricane rebuilding. Strong corporate profits provided both the business confidence to invest as well as a source of funding.

However, the peak of the current nonresidential building cycle has passed. The economy will slow in 2007 leading to reduced corporate profits, slower absorption of properties and stabilising utilisation rates. Construction of retail structures seems particularly exposed as reduced homeowner equity removes some of the impetus that has fuelled consumer spending in recent years.

Our second graph, showing trends in some of the key non-residential construction sub-sectors, illustrates the cyclical nature of construction investment and provides a window on the expected path for key commercial and manufacturing segments. The peak of the current cycle appears to have come last year, and this building cycle has been less pronounced than others.

The good news is that the reduced scale of the upturn provides an opportunity for a prolonged period of real spending growth, which will be weaker than that recently experienced, but which avoids a significant downturn.

Canada

Canadian economic growth will slow in tandem with the US in 2007, due to their close ties and also due to lower energy prices and higher interest rates. The last few years has seen the Canadian economy running close to its capacity, which generated strong non-residential construction activity in 2006. However, as slowing growth creates slack, the impetus for further investment will taper off.

Canada's housing market had less speculative activity than was seen in the US, and while residential investment will contract about -5% in 2007, it will not see the magnitude of the correction the US will experience - about -14%. Canada's growth will be concentrated in British Columbia and energy-rich Alberta, while the centre and east of the country show modest gains at best.

Mexico

Mexican output growth, on the other hand, will remain relatively robust in 2007. The economy should continue to benefit from relatively lower interest rates with manufacturing and commerce leading the expansion. High world oil prices continue to boost government revenues and will allow increased public investment of +23% this year.

Strong investment rates have boosted the ratio of investment to GDP from +19% to +21% in Mexico since 2004. However, this is still low, and unless new and better infrastructure is provided to the economy, capacity restrictions will preclude a higher economic expansion.

North America represents the world's largest construction market. It offers good opportunity, but those doing business need to be aware of significant changes in the outlooks for key segments of the market and make the necessary allocations of their resources.